Compliance and Regulatory Alerts, Bates Research | 01-23-20

FINRA Reorganizes for More Coordinated Exams, Highlights Priorities for 2020

In his cover note accompanying FINRA’s annual Risk Monitoring and Examination Priorities letter, FINRA President and CEO Robert Cook (pictured) reminded members of significant enhancements to the examination program going forward.

Mr. Cook first described the recent reorganization of member firms into one of five business model categories: Retail, Capital Markets, Carrying and Clearing, Trading and Execution and Diversified This consolidation permits FINRA to assign each firm “a single point of accountability” that will have the “ultimate responsibility” for risk monitoring, assessment and “planning and scoping of exams tailored to the risks of the firm's business activities.”

Second, Mr. Cook highlighted the organization’s extensive efforts in preparing firms to comply with new regulations—particularly Regulation Best Interest (“Reg BI”)—that will be examination priorities for FINRA in 2020. To that end, he underscored the letter’s inclusion of practical questions that firms should consider in order to “assess and, if necessary, strengthen their compliance, supervisory and risk management programs.”

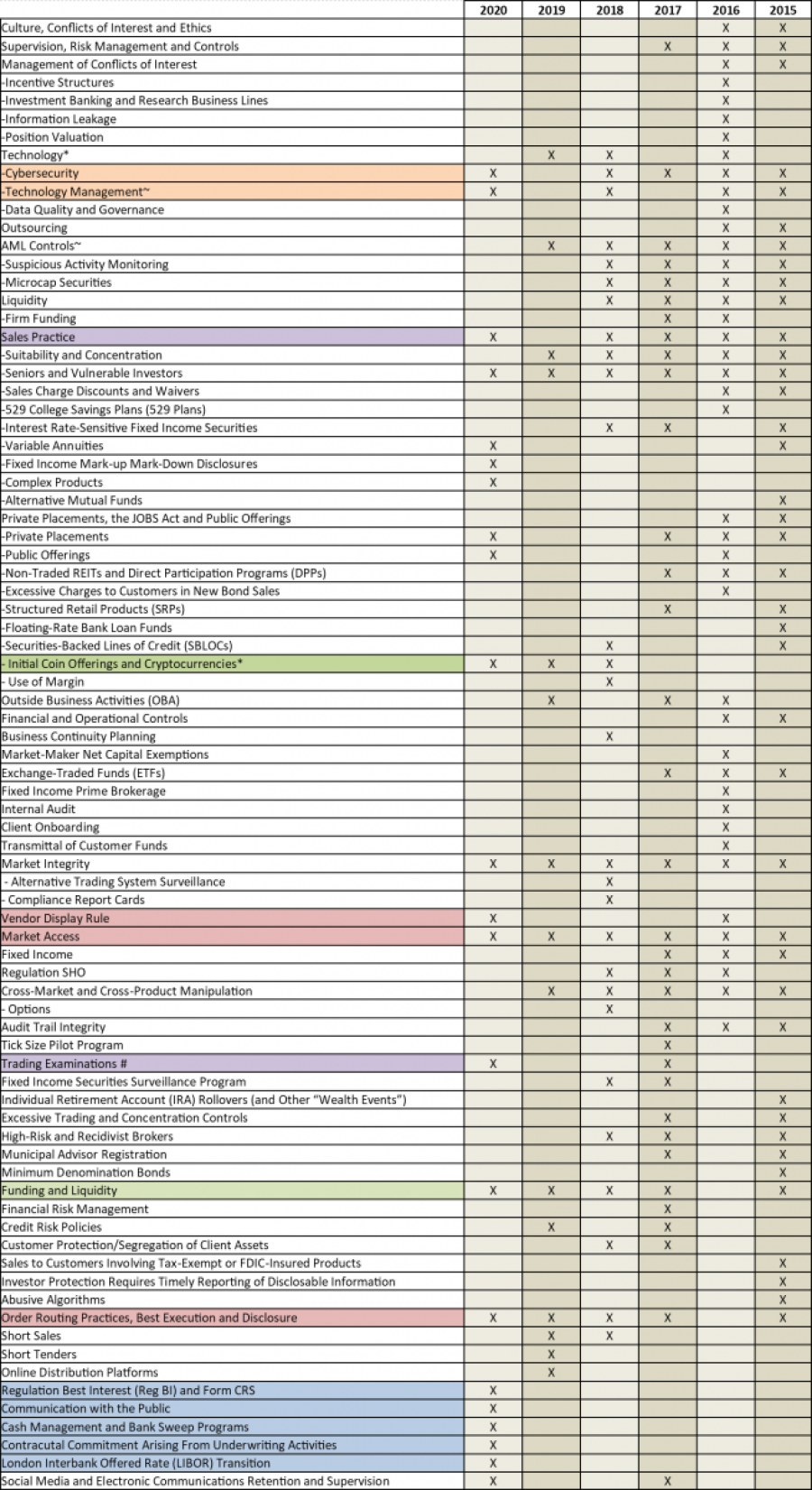

Top FINRA Exam Priorities for 2020

See highlights of FINRA’s continuing and emerging concerns on our 2020 FINRA chart below, which keeps track of articulated priorities from year to year.

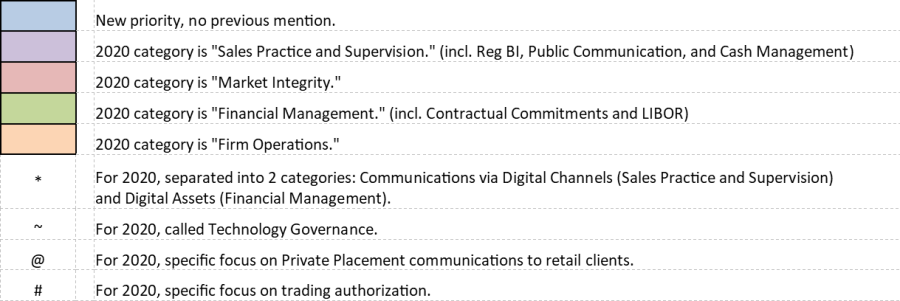

Legend

Source: 2020 FINRA Regulatory and Examination Priorities Letter (Compiled by Alex Russell, Managing Director)

Reg BI Tops the List

Reg BI was front and center in this year’s letter. FINRA emphasized that it will continue to offer transition resources as it “reviews firms’ preparedness” prior to Reg. BI’s June 30 implementation date. After that date, however, FINRA will examine broker dealers for compliance with the new regulation, the corresponding interpretations and the new Customer Relationship Summary (“Form CRS”) requirement.

Specifically, FINRA stated it will consider in its examinations whether: (i) adequate processes and procedures are in place to assess broker dealer best interest recommendations; (ii) the firm and associated persons are applying those standards; (iii) account monitoring adequately applies to both explicit and implicit hold recommendations; (iv) recommendations to retail customers are following “express new elements of care, skill and costs;” (v) customer recommendations take into consideration reasonably available alternatives; (vi) controls are in place to prevent excessive trading; (vii) adequate disclosures are provided for; (viii) conflicts of interest are adequately covered in policies and procedures; and (ix) filing and delivery of Form CRS is adequately addressed.

Sales Supervision and Communications

FINRA reiterated past priorities, saying that it will examine supervisory obligations over the sales of complex products (private placements, variable annuities and certain fixed income products). In 2020, FINRA highlighted that it will look closely at private placement retail communications to see how firms are fulfilling their supervisory obligations when using digital platforms (texting, messaging, social media or other applications). The letter states that FINRA will consider whether private placement communications are fair, reasonable and not misleading and whether they omit material facts, adequately explain risks, or contain false statements or promises. In addition, FINRA said it will examine these communications to ascertain whether they fully explain issuer metrics or projections on performance.

On the use of digital communications tools, FINRA asks firms to review their practices and programs to ensure that a representative’s digital communications comply with review and retention requirements and to consider whether their supervisors can recognize—and follow up on—the “red flags” of unapproved communications channels.

Cybersecurity

FINRA states that “cybersecurity has become an increasingly large operational risk.” As a result, FINRA advises firms that it will examine policies and procedures to ensure that customer records and information are adequately protected. FINRA also reminded firms that cybersecurity controls should be appropriate to the firm’s scale of operations and business model. Specifically, the FINRA letter prods firms to consider their “technology governance programs” to determine whether they are “expose[d] to operational failures” that may compromise their ability to comply with a range of rules and regulations. In this respect, FINRA will evaluate the adequacy of firms’ business continuity plan to ensure that the firm has the procedures and capacity to “maintain customers’ access to their funds and securities, as well as manage back-office operations, to prevent delays or inaccuracies relating to settlement, reconciliation and reporting requirements.” FINRA stated that it will examine testing and for tracking information technology problems.

Additional FINRA examination priorities for 2020 include:

- Trading Authorizations – FINRA will examine whether firms have the systems and supervision in place to address trading authorizations, discretionary accounts and key transaction descriptors. This includes whether firms can detect and address registered representatives exercising discretion without written client authorizations.

- Bank Sweep Programs – FINRA will examine a broker dealer’s use of bank sweep programs (sweeping investor cash into partner banks or mutual funds) to ensure that such services are not misrepresented, and that any program arrangements as well as cash management alternatives are adequately communicated to the customer.

- Digital Asset Investments – For firms that are considering engaging in digital asset investment activities, FINRA will examine whether they are filing the appropriate documentation for engaging in such activity, and whether their marketing and retail communications present a fair and balanced look at the risks presented. FINRA is also concerned with technology-related risk and cautioned that it will review automated systems associated with market access (such as monitoring for trading behavior, adjustments to credit limit thresholds, third party vendors and training).

- IPO Practices – FINRA will examine a firm’s compliance with rules restricting the purchase and sale of initial equity public offerings, and on new issue allocations and distributions. FINRA wants firms to review their practices and procedures to ensure that (i) they can adequately detect and address issues of “flipping” or “spinning;”(ii) IPO allocation methodologies and “calculations of aggregate demand” are fully explained; (iii) there are adequate controls to prevent allocations to restricted persons; and (iv) the firm records and verifies information for customers receiving these allocations.

- Best Execution – FINRA will continue to focus on compliance with best execution rules as they pertain to routing decisions and procedures for the handling of odd lots, treasuries and options (all subjects of enforcement actions in 2019). Further, FINRA said it will review processes related to handling of customer orders, including how the firm addresses conflicts of interest concerning now prohibited types of remuneration.

FINRA will also continue to examine priorities highlighted in the past, including adequate supervision and compliance over anti-money laundering and fraud, insider trading and manipulation across markets and products.

Conclusion

The priorities contained in this year’s FINRA letter are consistent with those contained in the annual report issued by the SEC’s Office of Compliance Inspections and Examinations (see recent Bates coverage). Similar to the OCIE report—which should be considered in tandem with this letter—the FINRA priorities emphasize the importance of firms preparing for Reg. BI and, more generally, for addressing vulnerabilities in compliance programs and practices. FINRA’s recent consolidation and reorganization and the identification of a “single point of accountability” should prompt firms to engage with them sooner, particularly over preparations for Reg BI, to ensure they are moving toward full compliance with these priorities.

For more information concerning Bates Group's Practices and services, please visit:

Broker-Dealer Compliance Services

Retail Litigation and Consulting

Regulatory Enforcement and Internal Investigations

Bates Investor Risk Assessment for Vulnerable and Senior Investors